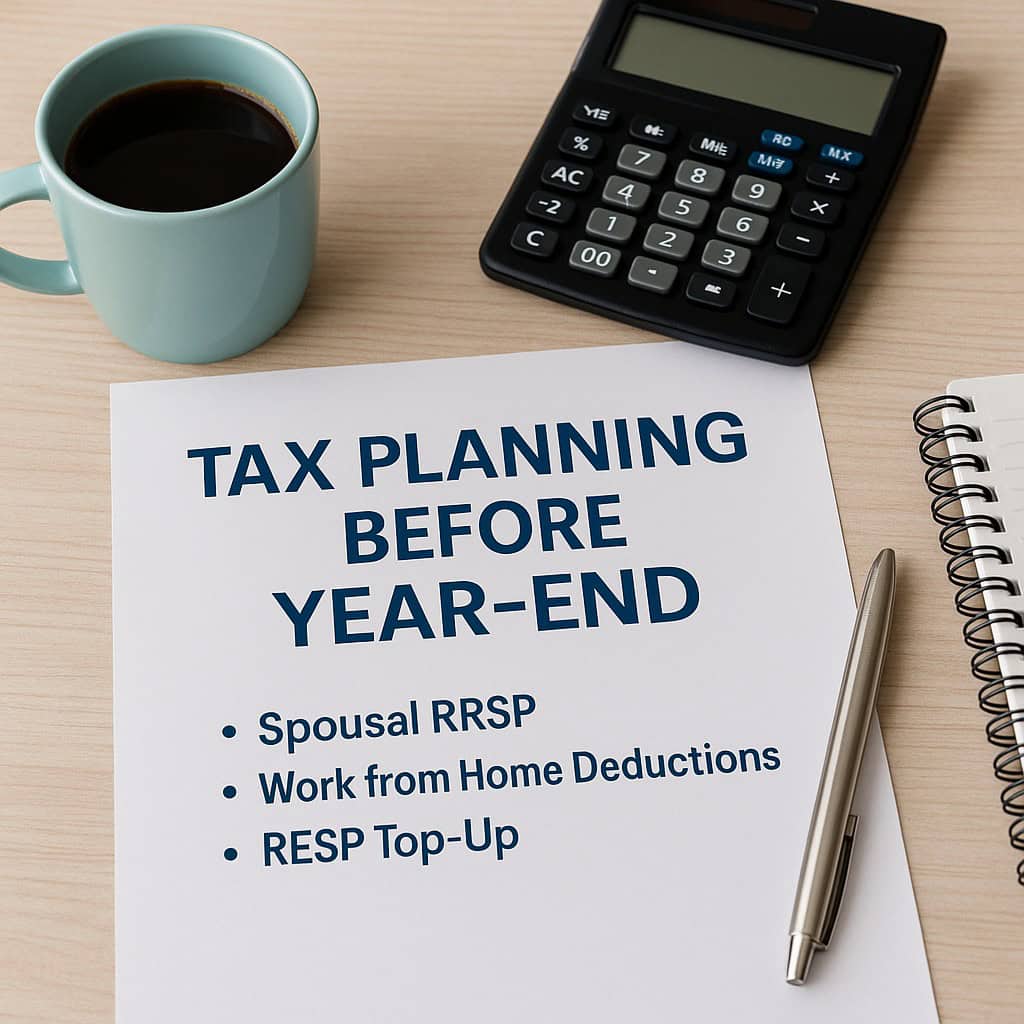

Tax Planning Before Year-End: Don’t Leave Credits on the Table

As the year winds down, it’s the perfect time to focus on year-end personal tax planning in Canada.

While most people wait until filing season to think about taxes, the smartest savings happen before December 31.

A few intentional steps now, like optimizing RRSPs, home-office claims, and RESP contributions, can mean hundreds or even thousands saved when you file next spring.

This guide covers three essential year-end tax strategies that help Canadians maximize credits and reduce their 2025 tax bill.

1. Make the Most of a Spousal RRSP

A Spousal RRSP is one of the best tools for year-end personal tax planning in Canada, especially for couples with different income levels.

It allows you to split income strategically, lowering household taxes now and in retirement.

How it Works

-

The higher-income spouse contributes to the Spousal RRSP in the other’s name.

-

The contributor gets the tax deduction, reducing taxable income for 2025.

-

The lower-income spouse owns the account and will pay less tax when withdrawing funds later.

Example:

Taylor earns $100,000; Jordan earns $40,000. Taylor contributes $5,000 to Jordan’s Spousal RRSP before the February 29, 2026, deadline. Taylor’s 2025 income drops by $5,000, saving about $1,900 in taxes, and future withdrawals are taxed at Jordan’s lower rate.

💡 Pro Tip:

-

Make the contribution before year-end if you expect a lower income next year, the deduction is worth more today.

-

Contributions are allowed until the year your spouse turns 71.

-

Combine this with your regular RRSP strategy for a long-term retirement balance.

2. Claim Work-from-Home Deductions

Since 2020, millions of Canadians have worked remotely at least part of the year, and work-from-home deductions remain a key part of year-end personal tax planning.

Two Claim Options

-

Flat-Rate Method:

-

Claim $2 per day worked from home, up to $500 total, no receipts needed.

-

-

Detailed Method:

-

Deduct a portion of home expenses (utilities, rent, internet, and supplies) based on workspace size and use.

-

Requires Form T2200 signed by your employer.

-

Example:

If you used 20% of your home for work and paid $2,000 in annual utilities, you could deduct $400.

Even modest claims like this add up, especially for dual-income households.

What You Can Claim

✔ Utilities (electricity, heating, water)

✔ Rent or a share of condo fees

✔ Internet, office supplies, minor repairs

Not deductible: mortgage payments, property taxes (unless self-employed), or home insurance.

💡 Pro Tip: Keep bills and workspace notes. CRA may request proof during reviews.

3. Top-Up Your RESP Before December 31

The Registered Education Savings Plan (RESP) is one of the best year-end moves for parents or grandparents.

It’s not only a tax-advantaged savings vehicle but also offers free government matching through the Canada Education Savings Grant (CESG).

How It Works

-

The government matches 20% of your annual contributions, up to $500 per child per year.

-

Missed a year? You can catch up by contributing $5,000 to earn a $1,000 grant.

Example:

Contribute $2,500 before December 31 and receive a $500 grant automatically. That’s a guaranteed 20% return before investing a single dollar.

💡 Pro Tip: Even smaller contributions earn matching, if you can’t do $2,500, top up with whatever amount fits your budget to secure a proportional grant.

Bonus Move: Don’t Forget Donations and Medical Credits

Year-end personal tax planning also means reviewing charitable donations and medical expenses before the cutoff date.

-

Donations made by December 31 earn tax credits worth up to 50%.

-

Combine all family medical expenses on the lower-income spouse’s return to reach the CRA’s threshold faster.

These simple reviews can turn overlooked receipts into meaningful tax savings.

Why Year-End Personal Tax Planning in Canada Matters

Waiting until tax season often means missed opportunities.

The CRA’s rules are calendar-based, meaning most credits and deductions reset on January 1.

Strategic planning in November or December lets you:

✔ Lower your tax bill before it’s locked in

✔ Improve household cash flow

✔ Start 2026 ahead, organized and confident

Ready to Keep More of What’s Yours?

Don’t leave money on the table this year.

👉 Book a Year-End Tax Review to make sure every dollar is working in your favour.

We’ll walk through your situation, highlight deductions you might be missing, and help you plan for 2026.

💬 Referral Reminder

Do you know someone who could benefit from this kind of clarity?

Refer them to INDep Accounting and get 5% off your next return once they become a client.

Because good advice, and good results, are worth sharing.