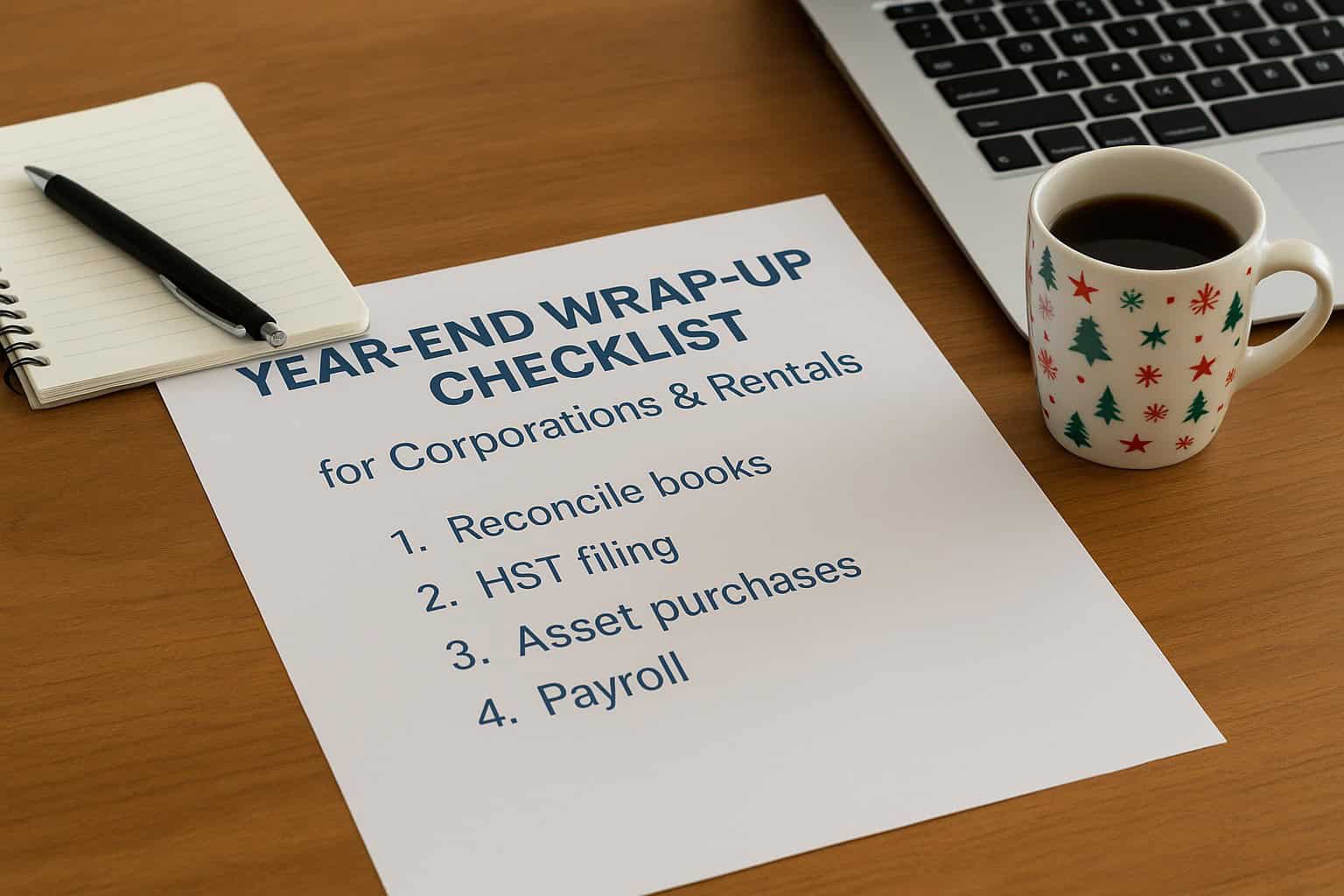

Year-End Wrap-Up Checklist for Corporations & Rental Businesses

As the year winds down and people across Canada take time to pause, connect, and celebrate the season in ways meaningful to them, it’s also an important moment for business owners and rental property investors: year-end planning.

Proactive preparation now helps you avoid CRA surprises, reduce stress, and position your business or rental operation for a strong start to the coming year. Here’s a clear, practical checklist to guide you through what matters most before December 31.

1. Reconcile Your Books to Year-End

Accurate books are the foundation of a smooth tax season.

Before year-end, ensure all accounts are fully reconciled, including:

- Business bank accounts

- Credit cards

- Rental property accounts

- Loan and line of credit statements

- PayPal/Stripe/Square

Why it matters:

Reconciliation errors cause missed deductions, incorrect tax filings, and unnecessary CRA inquiries. Cleaning things up now ensures accuracy later.

💡 Quick Tip:

If a transaction is still uncategorized or missing, resolve it before December 31. The CRA expects accurate year-end balances.

2. Prepare for HST/GST Filings

Most corporations and rental businesses filing short-year or December year-end periods must ensure sales tax filings are up to date.

Confirm:

✔ All HST collected is reported

✔ All eligible Input Tax Credits (ITCs) are claimed

✔ Special rental rules (e.g., short-term accommodations) are applied correctly

Why it matters:

CRA penalties for incorrect or late HST filings can add up quickly — especially for businesses collecting more than one sales tax type throughout the year.

💡 Rental Tip:

If you collected HST on short-term rentals, ensure your bookkeeping separates taxable vs. exempt rental periods.

3. Review Asset Purchases & Depreciation Before Dec 31

Corporations and rental property owners may benefit from purchasing qualifying assets before year-end to maximize capital cost allowance (CCA) or immediate expensing opportunities.

Examples include:

- Computers, equipment, and tools

- Vehicles

- Rental property appliances

- Renovations (capital improvements)

- Security systems

- Office furniture

Why it matters:

CCA (depreciation) can only be claimed on assets available for use before year-end. Even a partial year counts.

💡 Tip:

If you plan to buy equipment early next year, consider moving the purchase to December instead — the tax benefits may arrive faster.

4. Finalize Payroll, T4s, and Remittances

If your corporation pays employees or pays you a salary, confirm that:

✔ December payroll is processed

✔ All remittances are made on time

✔ Bonuses are recorded before December 31 (if applicable)

✔ Vacation payouts or adjustments are posted

✔ Records of Employment (ROEs) are updated (if needed)

Why it matters:

Payroll corrections after year-end often require amendments and can delay tax filings.

💡 Owner Tip:

If you pay yourself a salary, review your salary vs. dividend mix for 2025. The right combination can build RRSP room, optimize CPP, and reduce your overall tax burden.

5. Confirm Rental Income & Expenses

For rental property owners:

✔ Ensure all rent collected is recorded

✔ Track utilities, repairs, insurance, mortgage interest, and condo fees

✔ Separate capital upgrades from maintenance costs

✔ Keep receipts for all property-related expenses

✔ Prepare summaries for each rental unit

Why it matters:

CRA rental reviews are increasingly common. Organized records protect you and maximize deductions.

💡 Pro Tip:

If you renovated this year, categorize expenses properly. Improvements increase the property’s value and may not be fully deductible this year.

6. Review Shareholder & Owner Transactions

Before the year closes, corporations should always review:

- Shareholder loan balances

- Reimbursements and business expenses paid personally

- Dividends issued or planned

- Adjustments required for year-end

Why it matters:

Improperly managed shareholder loans can result in taxable benefits — an unwelcome surprise at filing time.

7. Book Your Year-End Review

Many year-end opportunities disappear once the calendar flips to January. A professional walkthrough helps you:

✔ Catch missed deductions

✔ Identify planning opportunities

✔ Prepare for corporate or rental filing

✔ Avoid penalties

✔ Start the new year with clarity

👉 Book Your Year-End Strategy Call

💬 Referral Reminder

Do you know someone who could benefit from this kind of clarity?

Refer them to INDep Accounting and get 5% off your next return once they become a client.

Because good advice and good results are worth sharing.